The Iran War Is Not 2022

Markets are panicking. Everyone sees 2022 again. The chart setups look almost identical and the energy shock is real. But the comparison falls apart under scrutiny. The macro is different, and the oil disruption is transitory.

Historically, military conflicts are buying opportunities.

Despite this historical edge, the 2022 comparison has the market's attention. The aftermath looks eerily similar: major energy disruptions, geopolitical shifts, and nearly identical chart patterns across assets — bitcoin being the most striking example.

In 2022, risk assets bottomed on the day of the Russian invasion (February 24th). Yet the subsequent bounce was a bull-trap, and by late March markets had resumed crashing. The true driver of that Q2 crash wasn’t the war, but a hawkish Federal Reserve forced to hike into rampant inflation (which the oil spike made worse).

But the 2022 playbook does not apply here, for two reasons: the macro, and the oil shock.

The Macro: No Hawkish Fed

Today’s macro environment is entirely different from 2022’s.

In 2022, the Fed was behind the curve and about to begin its steepest relative hiking cycle in history, with YoY inflation already at 7.9% and the real Fed Funds Rate at a stunningly negative -7.5% when the war started.

Today, the Fed is in a position of strength and in wait-and-see mode, with a real rate of +1.2% and inflation trending lower.

Even if the oil spike pushes headline inflation temporarily higher, the Fed has room to look through it. At +1.2% real rates, they don't need to tighten into a supply shock. In 2022 they had no choice — at -7.5% they were catastrophically behind. That's the difference that matters for risk assets.

The Fed’s own framework favors inaction. Williams said oil prices would affect the “near-term inflation outlook” but that the Fed would need to “assess persistence”. That is code for: we’re not moving unless this lasts. The U.S. economy is also far less oil-dependent than it was in the 1970s or even 2008, meaning the pass-through from crude to core inflation is weaker than the headline spike suggests. Treasury Secretary Bessent made a similar point: the U.S. is "in a very different position than when Russia invaded Ukraine."

Since the strikes began, four Fed officials have spoken publicly. None altered their outlook. Williams called the market reaction “muted.” Kashkari said it’s “too soon to know” the impact and still sees one to two cuts this year if inflation cools. Hammack, a known hawk, called the current policy stance “neutral” and urged an extended pause. The Fed is telling you in plain English: we’re not reacting to this.

The Oil Shock: Less Persistent

2022: A Structural Shock

When Russia invaded Ukraine, Europe lost access to roughly 4.5 million bpd of Russian crude and refined products — about 3.2 million bpd of crude and 1.3 million bpd of products. It was the largest commodity dislocation since the 1970s. And Western sanctions made the disruption permanent: Russia’s share of EU petroleum imports went from 30% to under 3%.

Russian oil found new buyers in India and China at steep discounts, but the rerouting was slow and messy — longer voyages, strained tanker capacity, spiking freight rates, and a shadow logistics network built from scratch. This chaos hit a market running on fumes: global inventories had been drawing for five consecutive quarters.

Brent peaked near $130 on March 8 and didn’t break below $90 until late August. Six months of elevated prices because the plumbing needed to move them took half a year to rebuild. The shock was structural, not transitory.

2026: A Transitory Disruption

Iran produces roughly 3.3 million bpd and was exporting about 1.9 million bpd before the strikes — almost entirely to China through shadow fleet channels at $11-12/bbl discounts to Brent, with 87% of its tanker fleet already sanctioned by the U.S. Additional sanctions on Iran post-war would change nothing.

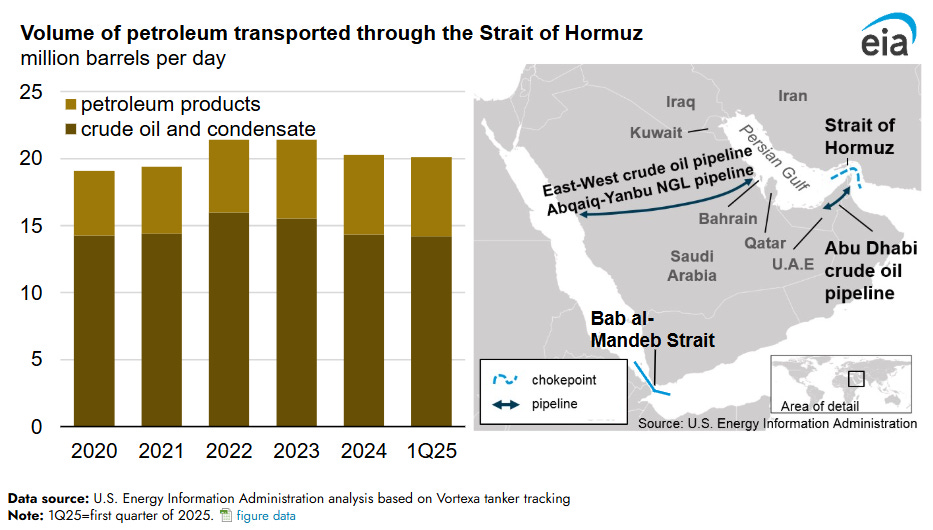

But Iran’s own barrels are not what has the market’s attention. The real disruption is the 14 million bpd of crude that transits the Strait of Hormuz, roughly 20% of global petroleum liquids consumption, where traffic has dropped almost to a standstill.

And yet the market response has been a fraction of 2022’s. Because the only thing blocking the flow is the war itself. End the war, the oil moves. And the U.S. controls the off-switch. Trump has projected a four-to-five week timeline. He has also just ordered the DFC to provide political risk insurance for tankers transiting the Gulf, plus Navy escorts if necessary, to restart shipping flows.

With nearly 60% of Americans disapproving of the strikes and midterms approaching, political incentives strongly favor a short engagement.

And unlike 2022, the market entered this shock in surplus — the IEA projected an oversupply of nearly 4 million bpd for 2026, global inventories were at a four-year high, and China had been stockpiling crude at roughly 900,000 bpd through most of 2025. The shock is transitory, not structural.

The Curve Tells the Story

The crude oil futures curve reinforces the point. Comparing the curves of January with March captures both the front-running and the shock itself, and the divergence is stark.

2022: front month repriced +42%, tenth contract +21%. The whole strip moved because the market understood rewiring supply chains would take quarters, not weeks.

2026: front month repriced +28%, tenth contract just +12% — despite a shock affecting 4.4x more barrels. Deferred contracts have barely moved because the market sees an expiration date to the supply shock.

Note: This chart shows the CL forward curve. The Brent forward curve shows nearly identical moves across both periods.

The Tail Risk

Iran has already struck Ras Tanura, Fujairah, and Qatari LNG facilities — so far mostly debris from intercepted drones, but the targeting pattern is escalating toward energy infrastructure. Gulf state interception rates are high but not perfect, and Iran reportedly has tens of thousands of drones in reserve. If direct hits start landing on refining capacity — SAMREF, Jebel Ali, Jubail — that is lost production that does not come back with a ceasefire. Refineries take months to repair. And the risk is no longer limited to oil. This is becoming a products and gas crisis, not just a crude problem. QatarEnergy has shut down LNG production at Ras Laffan and Mesaieed, removing roughly a fifth of global LNG export capacity.

What matters next: whether serious negotiations emerge, whether Iranian strikes begin consistently penetrating Gulf air defenses rather than being intercepted, whether refining outages start accumulating beyond precautionary shutdowns, and whether Trump’s four-to-five week timeline starts to slip. If the back end of the futures curve starts repricing — e.g., if that tenth contract moves from +12% toward +25% — the market is telling you the shock is turning structural.

But as of today, the curve hasn’t blinked.

Don’t confuse a transitory geopolitical shock (2026) with a major liquidity crisis (2022).

This is not 2022.

Lol, this analysis doesn't jive to well with military reality. Iran is winning and will win. The US can't open of Hormuz and can't protect any middle east nation from the Iranian missiles. Trump is an idiot and has nutcase religious fanatics advising him.

Really glad you are on Substack now!

X is so noisy!