The Mechanics of the Fed’s RMP Program

Why RMP is not QE

The Fed just committed to buying $40 billion in Treasuries every month, and the market is already screaming “QE!”

While the headline number looks like stimulus, the mechanics tell a different story. Powell isn’t trying to juice the economy but rather trying to prevent the plumbing from seizing up.

Here is a look at how the Fed’s Reserve Management Purchases (RMP) structurally differs from Quantitative Easing (QE), and its implications.

What is Quantitative Easing (QE)?

To strictly define QE, and distinguish it from standard Open Market Operations, the following conditions are required:

The Three Mechanical Conditions

The Mechanism (Asset Purchases): The central bank purchases assets, typically government bonds, using newly created reserves.

The Scope (Large-Scale): The volume of purchases is significant relative to the total market size, intended to flood the system rather than fine-tune it.

The Target (Quantity over Price): While standard policy adjusts supply to hit a specific interest rate (Price), QE commits to purchasing a specific volume of assets (Quantity), regardless of the resulting interest rate.

The Functional Condition

Positive Net Liquidity (QE): The rate of asset purchases must exceed the growth rate of non-reserve liabilities (such as Currency and the TGA). The goal is to force excess liquidity into the system, not just supply needed liquidity.

What is Reserve Management Purchases (RMP)?

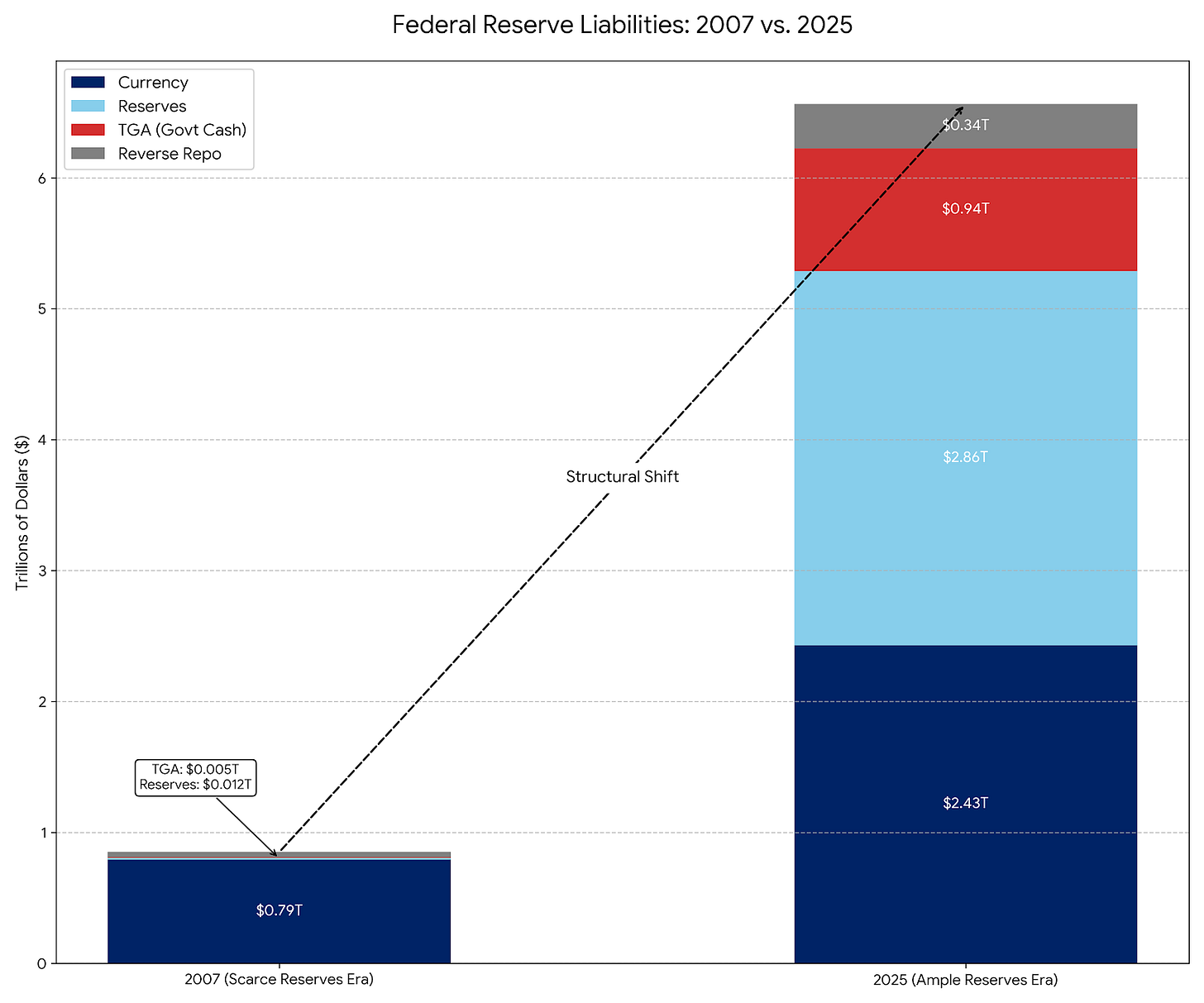

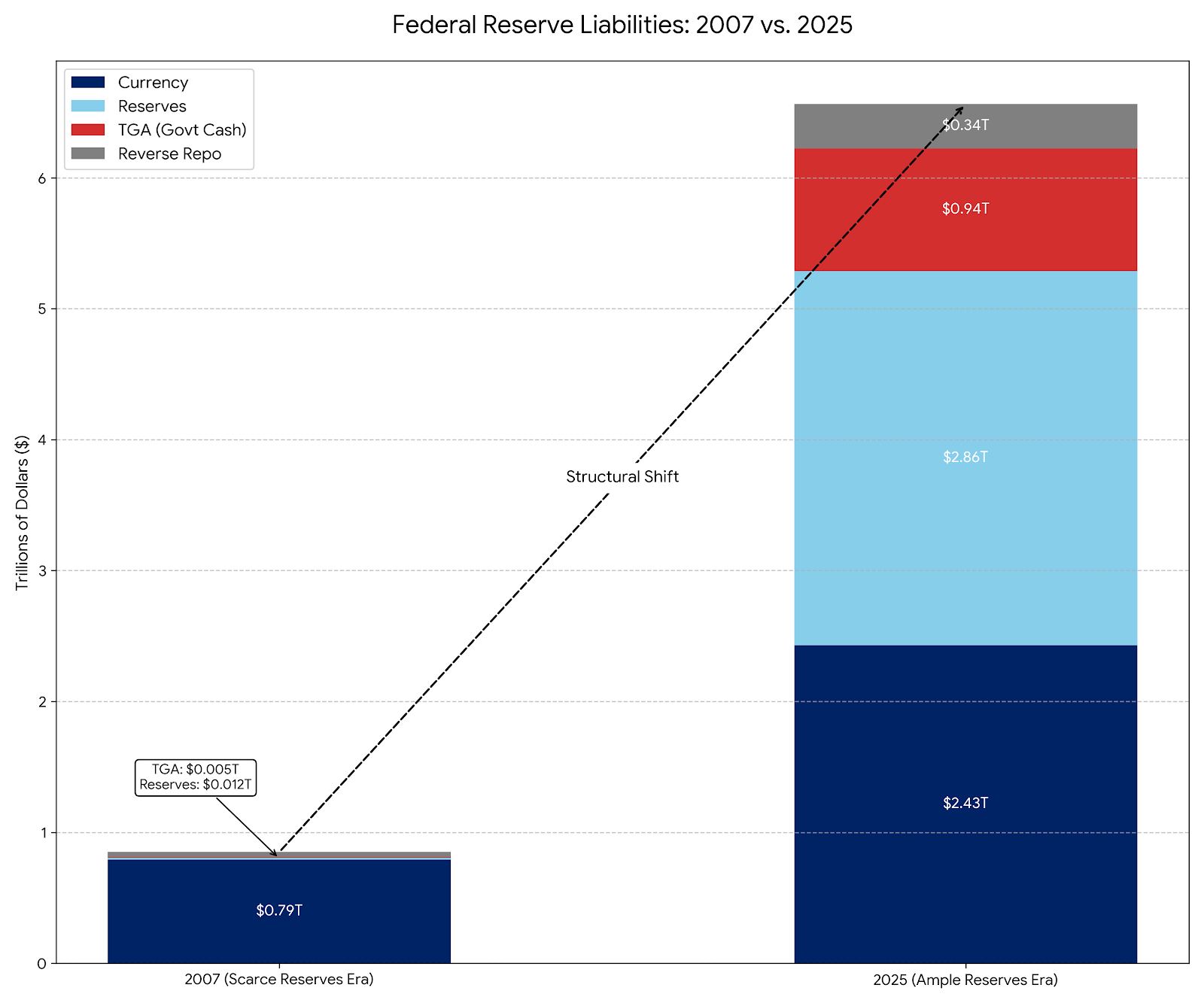

RMP is effectively the modern succesor to Permanent Open Market Operations (POMO), which was the standard operating procedure from the 1920s to 2007. However, the composition of the Fed’s liabilities has shifted drastically since 2007, necessitating a change in scope.

POMO (The Scarce Reserves Era). Prior to 2008, the Fed’s primary liability was physical currency in circulation; other liabilities were minimal and predictable. Under POMO, the Fed bought securities strictly to match the public’s gradual demand for physical cash. These operations were calibrated to be liquidity neutral and small enough that they did not distort market prices or suppress yields.

RMP (The Ample Reserves Era). Today, physical currency is a minor component of the Fed’s liabilities, which are now dominated by large, volatile accounts like the TGA and Bank Reserves. Under RMP, the Fed buys T-Bills to buffer this volatility and “maintain an ample supply of reserves on an ongoing basis.” Like POMO, it is designed to be liquidity neutral.

Why Now: The TGA & Tax Season

Powell implemented RMP because of a specific plumbing problem known as the TGA Drain.

The Mechanic: When individuals and corporations pay taxes (especially the major deadlines in December and April), cash (reserves) leaves their bank accounts and moves into the government’s checking account at the Fed (the TGA), which sits outside the commercial banking system.

The Impact: This transfer drains liquidity from the banking system. If reserves drop too low, banks stop lending to each other, causing a Repo Market crisis (like in September 2019).

The Solution: The Fed is launching RMP now to offset this drain. They are creating $40B in new reserves to replace the liquidity that is about to be sequestered in the TGA.

Without RMP: Tax payments tighten financial conditions (Bearish).

With RMP: Tax payments are neutralized (Neutral).

Is RMP actually QE?

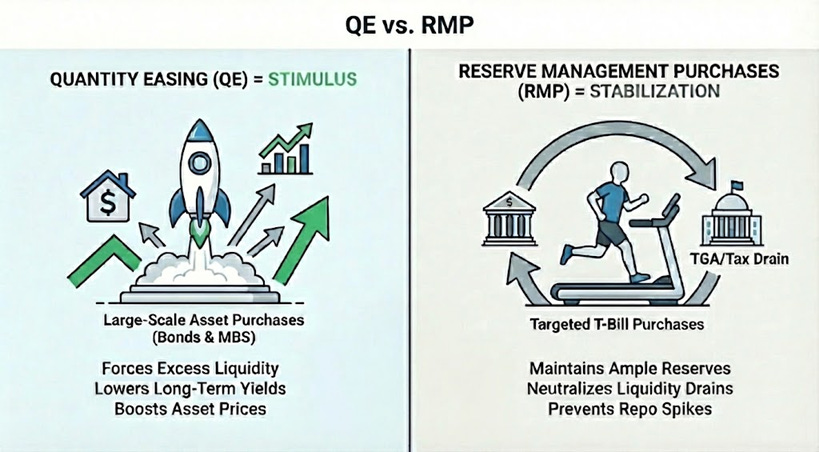

Technically: YES. If you are a strict monetarist, RMP is QE. It meets all three mechanical conditions: It is a large-scale asset purchase ($40B/month) using new reserves with a quantity target.

Functionally: NO. RMP acts as a stabilizer, whereas QE acts as a stimulus. RMP does not materially ease financial conditions but rather prevents them from tightening during events like the TGA refill. Because the economy naturally drains liquidity, RMP must run constantly just to maintain the status quo.

The Tipping Point: When does RMP become QE?

For the RMP program to cross the line and become full-blown QE, one of two specific variables must change:

A. The Duration Shift. If RMP begins buying Treasury Bonds or MBS, it becomes QE. By doing so the Fed removes interest rate (duration) risk from the market, lowering yields and forcing investors to reallocate into riskier assets, which boosts asset prices.

B. The Quantity Shift. If the organic demand for reserves slows (e.g., the TGA stops growing), but the Fed keeps buying $40B per month, RMP becomes QE. The Fed is now injecting excess liquidity that the plumbing doesn’t need, which will inevitably spill over into financial assets.

Conclusion: Market Impact

RMP is designed to prevent the liquidity drain from tax season from impacting asset prices. While technically neutral, its reintroduction sends a psychological signal to the market: The Fed Put is active.

The announcement is net bullish for risk assets. It represents a “mild tailwind.” By committing to $40B/month, the Fed has effectively placed a floor under banking system liquidity. This removes the tail risk of a Repo Crisis, emboldening leverage.

However, this is a stabilizer, not a stimulus. Because RMP merely replaces the liquidity being drained by the TGA rather than expanding the net monetary base, it should not be mistaken for the systemic easing of true QE.

I heard the metal of the printer crank last night. It sounded awfully familiar. I swear I could’ve heard it echo “Q…. E….”

Some important distinctions and nuances made here, and I would agree that if this is a temporary measure then it's not QE. However to play devil's advocate, I think about QE as growth of the Fed's balance sheet greater than trend of GDP and (as you say) non-interest bearing liabilities since the LSAPs (whether bonds, FX in China's case, or equities in SNB's case) need to be funded with reserve liabilities. To the extent new bills under RMP keep the balance sheet elevated, then i would argue it is QE as it keeps the balance sheet size from prior rounds elevated relative to trend, to which QT was normalizing. It could be to alleviate funding stress and TGA growth for tax season as the Fed is laser-focused on these spikes, but there is the risk that it becomes ongoing.